Securities-Backed Line of Credit

What Are Securities-Backed Line of Credit?

Securities-Backed Line of Credit (SBLOC) is a type of loan where you can borrow money against your securities, using the securities as the collateral. They are typically obtained from a bank or a firm with a taxable brokerage account. There are some restrictions to this type of loan; you cannot purchase, trade, or carry securities, along with paying off margin loans.

Allowed Accounts and Rules

By regulation rules and tax laws, you cannot pledge securities from retirement accounts (IRAs or 401(k)s) as collateral. Even if the account is allowed, many firms require two minimums to be approved for an SBLOC.

Portfolio Minimum: Firms may want your total portfolio to be a certain amount. They can be as low as $100,000 or even higher.

Borrowing Minimum: If the borrower is asking for too little to borrow, they may not be approved for an SBLOC, as they may require a borrowing minimum.

For Example: I went to Firm A to take out an SBLOC. My total portfolio is worth $200,000 and the minimum required amount is $100,000. I meet this requirement and move on to the next step, how much do I want to borrow? I ask to borrow $80,000 and the minimum required to borrow is $50,000. Therefore, I meet both requirements and I can proceed with the SBLOC.

Since the requirements are hefty, SBLOC isn't really for the average person. Their target audience are clients with substantial portfolios because using securities as collateral is volatile due to an unpredictable market, regulation rules, and administrative overhead.

Borrowing Maximum

Even if you meet the requirements, banks or firms may also only allow a certain percentage to be borrowed based on your portfolio composition. Let’s use an example from an article on Schwab, written by Chris Kawashima:

“...a lender may accept 70% of the value of stocks, mutual funds, and exchange-traded funds and more than 90% of the value of Treasury securities and cash equivalents”

What we can understand is that these percentages are evaluated differently from firm to firm. The credit limit is determined by portfolio composition and total portfolio value. However, the typical idea is that an SBLOC agreement allows you to borrow 50% to 95% of your asset values.

The Purpose of SBLOC

The primary use of SBLOC is taking advantage of tax deferral. Tax deferral is simply postponing the payment of income tax. So there are two main things that the borrower is looking for when they take out this type of loan:

Whenever an investor successfully sells a security, they will incur a taxable event. However, an SBLOC avoids the taxable event, as you’re receiving money from a firm or bank, but you’re using the securities as collateral.

If the borrower believes their investments will appreciate in the long term, an SBLOC won’t interrupt their long-term investments. It allows them to hold their position for longer since the borrower isn’t incurring a sale.

What Borrowers Avoid

Most borrowers want to avoid paying more than the loan interest and the extra fees they may have. Whenever the securities dip below the borrowed amount, the firm asks the borrower to add more money or assets as collateral. If they cannot, the firm will ask which securities to sell to make up for the loss. If the borrower doesn’t specify, the lender will sell any asset without further notice. Not only does the borrower lose some of their positions in the market, but they will also incur a taxable event.

Although this is easily avoidable, since the majority of the borrowers never borrow at the maximum credit limit. Typically their cushion is large enough where this never happens and they have a diversified portfolio where market downturns don’t hinder the total value as much. It’s also known that there is only a small percentage of borrowers, since they all have to have high profiles to meet requirements.

The Benefits of SBLOC

Let’s review what we’ve learned so far about the benefits of SBLOC:

Liquidity: You don’t have to sell your securities to obtain usable cash.

Tax Efficient: Not needing to sell your securities takes advantage of tax deferral.

Long-Term Benefits: Being able to hold your position on your securities allows for better long-term investments.

The Downsides of SBLOC

We already know that one of the biggest cons of SBLOC is actually needing to use your securities as collateral. However, one of the overslept dangers is the interest rates you have to pay. The interest rate actually fluctuates based on the market rates. So if the interest rate rises, the cost of carrying the loan will as well. Although, if you’re playing safe to begin with, it’s not too much to worry about since the interest rate is typically lower than other loans and you have a large cushion to fall on.

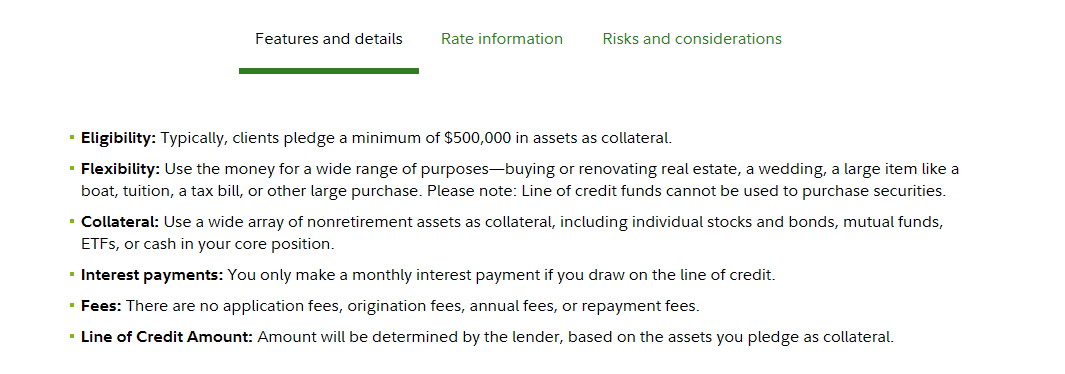

Real Life Example

Let’s look a Fidelity’s SBLOC Information:

We can see that borrowers must have a minimum of $500,000 and suggest having a wide range of assets as collateral. They even state the account can’t be a retirement account like we mentioned earlier. They also charge no application fees, origination fees, annual fees, or repayment fees. However, they could have other fees that may not be listed here. Like we said before, the maximum amount you can borrow is determined later based on your portfolio.

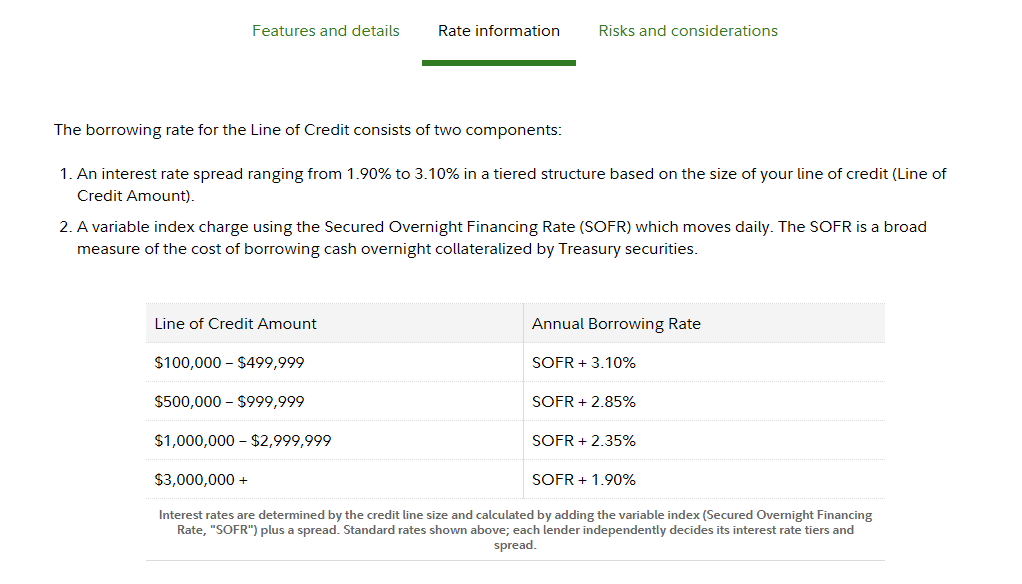

They even list their rates based on the line of credit you have. However, they also state the fluctuating rate known as Secured Overnight Financing Rate (SOFR), which is likely the rate we mentioned earlier that is linked with the market rate.

The Bottom Line

SBLOC is a great option for investors if they have the portfolio to back up their borrowings. They’re great for liquidity and keeping positions without incurring taxable events. Since not many people are eligible in the first place, it’s very unlikely you’d consider this option compared to Margin Loans or HELOC. Although those are inherently different from SBLOC, they have similar core concepts to SBLOC.

-

(April 2, 2026). What’s a securities-backed line of credit?. Fidelity. https://www.fidelity.com/learning-center/smart-money/what-is-a-securities-backed-line-of-credit

(January 3, 2024). Securities-backed Lines of Credit Explained. Finra. https://www.finra.org/investors/insights/securities-backed-lines-credit

(Retrieved June 23, 2026). Securities Backed Line of Credit. Fidelity. https://www.fidelity.com/lending/securities-backed-line-of-credit

Forbes. (November 29, 2021). How America’s Richest Can Access Billions Without Selling Their Stock. YouTube. https://www.youtube.com/watch?v=kDhtrogJ1Yo

Kawashima, C. (April 18, 2025). What is a Securities-Backed Line of Credit?. Schwab. https://www.schwab.com/learn/story/what-is-securities-based-lending

The Ernest Group. (Retrieved June 23, 2026). What is Tax Deferral? WellsFargo. https://fa.wellsfargoadvisors.com/ernst-group/What-Is-Tax-Deferral.c88.htm