Fees, Errors, and Returns

By Ethan Yan | April 19, 2026

When you purchase or sell a security, you should keep in mind its expense ratio and other fees that may come up with it. We often only think of the taxes we need to file when you earn dividends or capital gains, but we should also focus on the main three fees: Expense Ratio, Commission Fees, and Bid/Ask Spreads.

Expense Ratios and Hidden Fees

Expense Ratio

The annual rate that the fund charges for the total asset, in order to pay for its operating costs. It’s important to know the Expense Ratio for long term investments, as the fees will add up over time.

Their range varies; some are as low as 0.015%, while others can be as high as 10%. They correspond with the type of investment you purchase. For example, passive funds will have lower ERs, since they simply track an index. While other investments, typically active, try to beat the benchmark, or use up more resources to achieve a higher yield.

Typically ER is calculated daily, but you would divide the ER by 365 to get its daily rate.

Take a look at this spreadsheet I made that’s great for predicting what your IRA account could be. Click This to Download.

Commission fees

When you buy or sell an investment, there may be a small fee charged for doing so. Although most brokerage firms don’t charge anymore, you should still look it up if they do.

Commissions are a flat fee and really only matter when you’re actively trading. In a retirement account, it typically matters less, as you want to avoid actively trading your retirement and taking advantage of the tax forgiveness.

bid/ask spreads

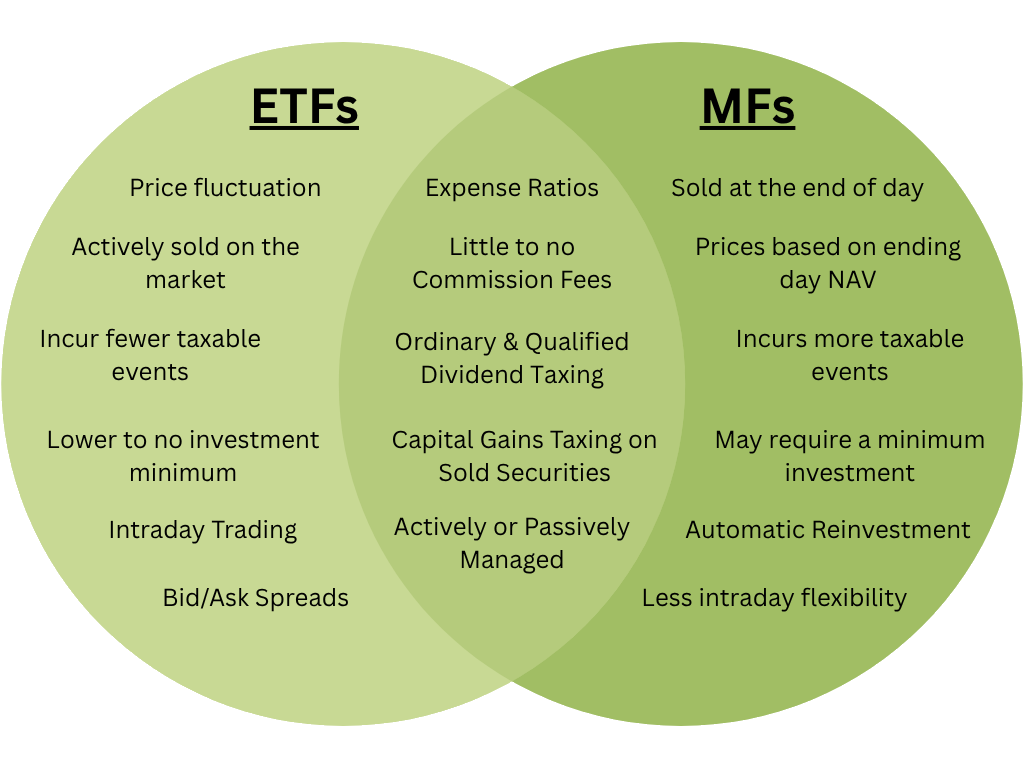

This really only applies to ETFs, stocks, or bonds, but not mutual funds.

When a buyer wants to purchase a security, they offer a bid price, the highest price they are willing to pay for that security. When a seller wants to sell a security they offer an ask price, the lowest they are willing to accept for that security. The discrepancy between these two prices create a Bid/Ask Spread.

When you want to trade a security immediately, you will likely pay slightly more or less than what you want because you’re paying a fee for immediately buying/selling at your closest bid/ask. I’ll also talk about this in a future blog, which will be linked here when it’s complete.

What you need to know is that when you trade the security, there’s a “hidden” fee of getting that security immediately.

Keep in mind that Commission Fees are mostly important in a brokerage account or in an active Roth IRA. Remember, with your IRA, you are probably better off not actively trading in it, but to focus on passive investments. Bid/Ask spreads don’t apply to mutual funds, as they don’t trade on the open market, but rather they are bought and sold at the end of the day at NAV.

Tracking Error in Index Funds & ETFs

Passive ETFs focus on tracking an Index, where its goal is to mimic the performance of that index. However, due to various factors, there will always be a discrepancy between the Index’s return and the ETF’s return. This creates a tracking error, which doesn’t correlate with the ETF’s performance, but rather its variability. It essentially lets the investor know that the ETF can be above or below the Index by a certain percentage.

There are multiple factors you should be aware about when dealing with tracking errors. Here I want to discuss Total Expense Ratio, Cash Drags, Rebalancing, and Timing. Typically passive funds will have small tracking errors (≤ 0.5%), while active funds will have larger tracking errors (≥ 2%) due to their aggressive nature.

Total expense ratio (Ter)

This is slightly different from just the expense ratio. The TER encapsulates every fee there is for the fund to operate.

What the TER does differently is provide an indicator on how much lag a fund’s return will be by that exact percent. This would be the best indicator if you held all things equal, but the reality is that it isn’t.

Cash drags

When dividends are incurred from underlying securities, but have yet to be distributed out to ETF shareholders, it creates a moment called Cash Drag. This is a moment where fund managers may reinvest the dividends temporarily or hold onto as cash reserves.

Reinvesting can reduce the cash drag, but the problem is that there are still transaction costs, longer execution timing, or other operation costs that come with it; this is known as friction.

Holding onto the dividends means you lengthen the cash drag, but the money not reinvested may miss market rises, therefore it reduces the friction but lengthens the cash drag.

Solution: Investors try to reinvest in batches to minimize both drag and friction costs.

Important thing to note: automatic reinvestment can reduce some drag on your end, but ultimately every investor will suffer from some cash drag.

rebalancing

Indexes can change over time, which forces portfolios to also change. For example, S&P 500 tracks the top 500 best performing companies in the US. When Nvidia rose to the top, many funds tracking the S&P 500 had to sell the lowest performing company and buy Nvidia stocks. The act of buying and selling has costs, causing friction, which creates a tracking difference.

timing

Indexes aren’t investments, they simply just track the performance of companies. So when changes happen to an index, it happens instantly. However, an ETF or Mutual Fund must sell and buy funds to these adjustments. Buying and selling these new securities takes a lot of time, which creates a tracking difference as prices can move during this waiting period.

Tax Efficiency of ETFs vs Mutual Funds

Some people believe that ETFs are better than Mutual Funds and vice versa. There are even people who believe that they’re virtually the same thing. They both serve their own purpose and although they are quite different, they are starting to blend in similarities.

I’ll say that it depends on your brokerage firm, as there are different incentives to use each one and they also have different policies when we’re talking about ETFs and Mutual Funds. I’ll try to focus on the majority of brokerages, but be sure to do more research on them with how they handle these qualities

Mutual Funds have a better edge than ETFs when investing passively in a retirement account. The main disadvantage of Mutual Funds is that it incurs more taxable events. However, if you’re investing in a tax-advantaged account, suddenly this isn’t a problem. Another bonus is that Mutual Funds have a longer history, making its longevity more trustworthy.

ETFs have a better edge in Brokerage Accounts. Since they inherently incur less taxable events, they’re great for non tax-advantaged accounts. On top of that, their liquidity makes them more attractive in these accounts since you can access the money at any moment. If you’re a more active trader, active ETFs can provide diversification, better capital gains, higher liquidity, and better transferability.

Dividends vs total returns

Dividends

Dividends are a portion of a company’s profits distributed out to its shareholders.

Although they’re great for investors, it doesn’t always mean that the company is performing well. Some companies will distribute dividends despite operating on a short-term loss, they do so to maintain the confidence in investors.

While this can be good, it can also be bad if they are too generous in dividends, as this could mean inefficient allocation in profits, as they aren’t reinvesting it into future growth.

total returns

Total Return is the amount made from an investment from the shareholder. It encompasses everything: dividends, interest, capital gains, and an increase in share price.

Within total return is the dividend adjusted return, which is the dividends and stock price appreciation.

Although it gives a better perspective of performance, it’s not a very good indicator of how the stock’s performance will be in the future. This is because the return is retrospective, where these increases could be from any reason.

So Total Return is better for investors who care about a stock’s performance over time. It is great for long term investments. However, if you want consistent ordinary income, the dividend yield is a better indicator for short-term performance. Keep in mind that these aren’t clear giveaways that a company is performing well. Investopedia writer Sean Ross says it best, “look at the company's balance sheet and income statement, and perform additional research as well” (Investopedia 13).

Concluding Thoughts

At this point, we should know a lot of the terminology. If you’re ever confused, I do recommend looking at my other blogs or doing your own independent research on topics/jargon I’ve covered in all of my blogs. Nonetheless, let’s quickly recap on what we’ve learned and what you should consider and look out for before investing.

Roth ira

Predominately invest in Passive Mutual Funds (Index Funds), with low Expense Ratios and Commission Fees. They provide consistent, stable, and automatic reinvestment.

When choosing your Index Fund, recognize that there will be discrepancies in your returns compared to the market index, due to cash drags.

Understand both the Dividend Yield and Total Return in these investments, as they can be good indicators of the company’s performance, which may mean it has a positive outlook in stable growth.

brokerage account

Focus on ETFs, whether it’s passive or active. Depending on your firm, you want to ensure you’re getting low commission fees and expense ratios. Look at the bid/ask spread to ensure you’re comfortable with the difference, which may be a key indicator in how liquid the stock is.

Returns may be lagging behind the market index, but this can be due to cash drag, so use other performance indicators like Dividend Yield or Total Return to gauge the company’s performance.

When choosing an Active ETF, be sure to check the market daily to capitalize gains. Passive ETFs can be treated like Mutual Funds in a retirement account, although you can still capitalize on gains when the time is right.

Although you can always do a lot of research, there is no guarantee that you will make money, especially in the short-term. However, there’s solid history behind Index Funds and Passive ETFs, so in the long-run you’re likely to make money. Keep in mind, this isn’t financial or investment advice. This is educational and preparation advice before you invest.

SOURCES

Doak, E. (February 13, 2025). ETFs Expense Ratios and Other Costs. Schwab. https://www.schwab.com/learn/story/etfs-how-much-do-they-really-cost

Ganti, A. (June 13, 2025). What is a Bid-Ask Spread, and How Does It Work in Trading? Investopedia. https://www.investopedia.com/terms/b/bid-askspread.asp

Hayes, A. (June 25, 2025). Total Expense Ratio (TER) Definition and How to Calculate. Investopedia. https://www.investopedia.com/terms/t/ter.asp

Ross, S. (February 26, 2026). Dividend Yield vs. Total Return: Which Matters More? Investopedia. https://www.investopedia.com/ask/answers/111314/which-more-important-dividend-yield-or-total-return.asp

Simpson, S. (October 28, 2025). The Rise of Exchange-Traded Funds: A Historical Overview. Investopedia. https://www.investopedia.com/articles/exchangetradedfunds/12/brief-history-exchange-traded-funds.asp

(Retrieved April 14, 2026). Understanding tracking error and tracking difference for an ETF. Fidelity. https://www.fidelity.com/learning-center/investment-products/etf/tracking-error-and-tracking-difference